Private/hybrid cloud: medium-sized providers in Switzerland gain market share

New ISG study: Large system integrators are losing customers to smaller providers. At the same time, demand for managed and colocation services is increasing.

solutions are increasingly attracting customers from the large system integrators. The main reasons for this are lower prices, greater agility and innovative strength as well as a more personalized service. This was observed in the new comparative study "ISG Provider Lens Private/Hybrid Cloud - Data Center Services Switzerland 2024", published by the market research and consulting company Information Services Group (ISG).

The study also shows that managed hybrid cloud solutions are becoming increasingly important, as collaboration with various hyperscalers and the integration of existing applications have become complex challenges for many companies. In the study, ISG examined the portfolio and competitive strength of 67 IT service providers and product providers that are represented in the Swiss private/hybrid cloud market with services and solutions.

According to the ISG study, Switzerland is an important European market for managed hybrid/cloud services. In addition, the number of service contracts on the Swiss market is currently growing faster than in Europe as a whole. More than ever, SMEs are also increasingly in need of service providers with extensive management capabilities, automated orchestration and industry-specific platforms. According to ISG, midmarket service providers are increasingly coming into their own as they react more quickly and flexibly to this demand than the traditional large providers.

"Medium-sized providers in Switzerland are also better able to act and communicate with their customers on an equal footing," says Heiko Henkes, Managing Director and Principal Analyst at ISG. "They are also currently scoring points because they can respond more flexibly to the individual needs of their customers and offer more personalized support," says Heikes. Several takeovers and mergers have recently caused additional movement in the Swiss provider market.

Market trends

The growing demand for outsourced IT infrastructure solutions is driving the expansion not only of managed services, but also of colocation services, according to the ISG study. In Switzerland, banks, insurance companies, the healthcare sector and public administrations are increasingly relying on the services of colocation providers and moving their infrastructure to their data centers. There are many reasons for this, above all the improvement of operational security, adherence to compliance requirements and the rapid provision of secure network connections all over the world.

ISG therefore predicts that competition between providers of hybrid IT and colocation services in Switzerland will intensify as companies increasingly look for flexible and secure solutions.

According to the ISG analysts, hybrid cloud solutions are also gaining momentum in Switzerland because companies have now realized that existing applications usually do not run smoothly in a public cloud environment. This is why they often decide either to operate in colocation data centers or to migrate to a managed hosting model. With the current state of technology, service providers have the option of managing colocation, hosting and cloud via a central AIOps platform.

"Last but not least, the particularly high demand for so-called sovereign clouds in Switzerland has further fueled the private/hybrid cloud market in the country," says ISG analyst Henkes. "As more and more AI services find their way into companies, the volume and quality of data stored in the cloud is also increasing exponentially." This further enhances the role of the private cloud, as it is better protected from access as an encapsulated unit than public cloud models.

From the multi-cloud to the polycloud

According to the ISG study, hybrid and multi-cloud variants are now the most common approaches when choosing cloud models. They are also developing more and more in the direction of "polycloud", where the focus is on individual concrete services instead of comprehensive systems. The aim is for applications and services to have access to the best available services - be it an industry-specific cloud solution, a specialized database or a specific AI or ML service. "The polycloud is usually based on several public cloud providers that are combined with the private cloud," says Heiko Henkes. "This transformation is driving the current modernization of the IT infrastructure."

At the same time, cost optimization in the cloud is currently a top priority. According to the ISG analysts, Swiss companies have clearly aligned their goals towards cost reduction and efficiency. As a result of the rapid expansion of cloud usage in recent years, cloud spending has become one of the most important areas when it comes to reducing costs. In recent years, companies have achieved cost savings primarily through simple FinOps cloud management. Now, however, more fundamental structural reforms are on the agenda, for example using cheaper cloud-native technologies such as "serverless", in which servers are treated separately from app development.

Classifications

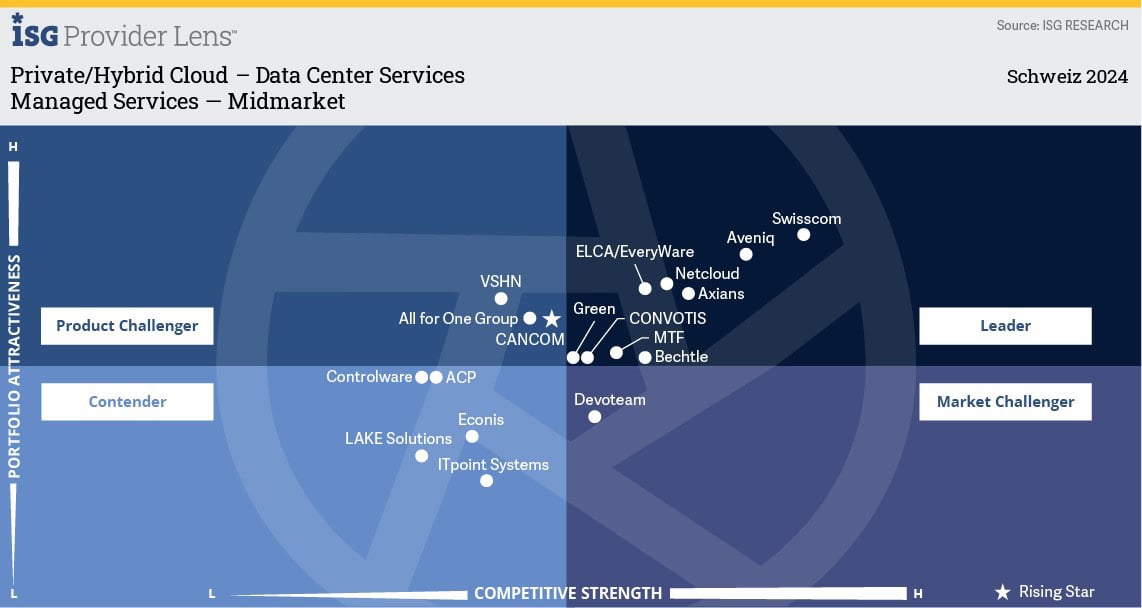

The study "ISG Provider Lens Private/Hybrid Cloud - Data Center Services Switzerland 2024" evaluates the capabilities of a total of 67 providers in five market segments (quadrants): "Managed Services - Large Accounts", "Managed Services - Midmarket", "Managed Hosting - Large Accounts", "Managed Hosting - Midmarket" and "Colocation Services".

The study classifies Swisscom as a "Leader" in all five market segments, while Atos, Aveniq, Bechtle, Convotis, ELCA/EveryWare, Green, Kyndryl, MTF and ti&m are described as "Leaders" in two quadrants each. Accenture, Axians, BitHawk, Capgemini, Digital Realty, Equinix, Netcloud, NTS Workspace, NTT GDC, Stack Infrastructure, TCS, T-Systems, UMB and Wipro are "Leaders" in one segment each.

In addition, Cancom, HCLTech and Rackspace Technology are each designated as "Rising Stars" in one quadrant. According to ISG's definition, these are companies with a promising portfolio and high future potential.

In the "Customer Experience" category, Green was named a global "ISG CX Star Performer 2024" among service providers of Private/Hybrid Cloud - Data Center Services. Green achieved the highest scores in the ISG Voice of the Customer survey in terms of customer satisfaction. The survey is part of the ISG Star of Excellence™ program, a leading quality competition for the technology and business services industry.

Source: www.isg-one.com