Sustainability with a system

The Federal Council is advocating mandatory sustainability reporting on respect for human rights and environmental protection for companies with over 500 employees in the parliamentary debate on the indirect counter-proposal to the Corporate Responsibility Initiative. How can companies deal constructively with these increased demands?

The following explanations are intended to show how companies are able to use a systematic approach to build up a solid database, identify concrete measures and also use this to communicate - without the risk of "greenwashing".

The ISO management system standards as a possible approach for companies

The approach according to the proven Deming cycle "Plan - Do - Check - Act" makes it possible to pursue a systematic procedure with countless topics. Sustainability management can also be set up in this way, whereby consistent attention must be paid to a continuous, coherent management system structure. For companies that are well acquainted with the ISO management system standards, it makes sense to build up an integrated management system that covers the three-dimensional concept and at the same time serves their own conformity and efficiency.

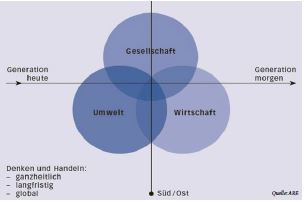

In this concept, sustainable development is represented by three circles for the target dimensions of environment, economy and society, supplemented by the time and north-south dimensions (see figure). This is intended to show the interconnectedness of economic, social and ecological processes, which influence each other. In addition, it is important to maintain solidarity with future generations as well as geographically with all people.

This could look as follows: Company X already runs a management system according to ISO 14001 and ISO 45001. It runs an ICS and has combined all company-relevant aspects in its risk management. It has a stakeholder analysis and detailed analyses of environmental and health hazards. Its monitoring system shows the progress of environmental and occupational safety performance, and targets for improvement are set regularly. Reporting is limited to a management review, which is used internally. A gap analysis is now a good way of identifying missing sustainability topics and indicators and supplementing the system on this basis. Stakeholder comments may also reveal additional sustainability aspects that are desired. The following (non-exhaustive) list shows examples of sustainability aspects that can be integrated into the management system, depending on their relevance for the company:

1) Society-oriented aspects:

- Respect for human rights

- No discrimination (race, ethnicity, religion, etc.)

- Education and training

- No child and forced labour

- Living wage

- Gender equality

- Freedom of negotiation and trade unionism

- rights of indigenous peoples

- Promoting local communities

- Safe communities and cities

- Improve the health situation

2) Environmental aspects:

- Climate protection

- Protection of biodiversity

- Ensure drinking water supply

- marine conservation

- Reduce chemical pollution

- Sustainable material cycles

3) Economic aspects:

- job creation

- Growth and poverty reduction

- No corruption

- No anti-competitive practices

- Creating efficient and resilient infrastructures

- Introduce sustainable production patterns

(Sources: ISO 26000 standard [not certifiable], SA 8000 standard, Sustainability Development Goals 2030 [UN], Global Reporting Initiative Standard, Planetary Boundaries Model, Federal Sustainability Strategy).

Application and consistency in the management system

Each of the aspects mentioned above can be managed with a "Plan - Do - Check - Act" approach. This requires appropriate indicators, goals that aim for continuous improvement, the measurement of actual conditions with the indicators and periodic reporting on them. For the latter, the management review report (MRB) is used in a management system. If the management system becomes a "sustainability management system", the MRB is transformed into a GRI-compliant sustainability report. In order to remain credible in terms of sustainable development, it is crucial that effective performance has been achieved, which is why it is not enough just to write a report - there must also be actual improvement and corresponding commitment behind it. In concrete terms, this means that the company management integrates the targeted sustainability aspects into its management and takes them seriously. This means that a thorough analysis (relevance to the company, opinions of stakeholders and shareholders) is needed at the outset, and from this a coherent derivation in terms of risks and opportunities. Only from such a consistently developed management system can a report be created that has sufficient substance.

The proposed approach in the current political environment

The Federal Council expects companies domiciled or operating in Switzerland to comply with international standards and principles of responsible corporate governance such as the OECD Guidelines for Multinational Enterprises, the UN Guiding Principles on Business and Human Rights and the UN Global Compact wherever they operate. These CSR principles should be further strengthened in the future. Regardless of whether the Corporate Responsibility Initiative or a possible counter-proposal to it will be successful before the Swiss people, public pressure on companies to comply with CSR will increase in the future. This is a direct consequence of increasing global media networking. With a proactive approach, a company maintains its freedom of action in this environment and achieves a positive public image.

Conclusion

Expectations of companies regarding CSR and sustainability will increase. A company that is strongly oriented towards ISO standards can use this to openly present its performance in the area of sustainability on the basis of its management system. Others can use selective tools along the "Plan - Do - Check - Act" cycle to track and communicate their sustainable development. In any case, however, it is advisable to pursue this disclosure only if a sustainable development of the company and its environment is actually aimed at. ■